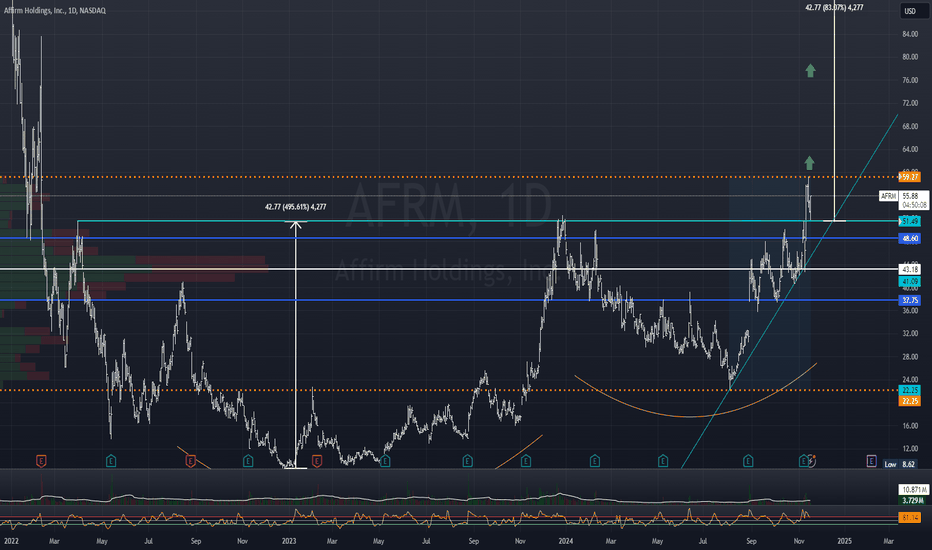

Affirm Holdings, Inc. (NASDAQ: AFRM), a leader in the buy now, pay later (BNPL) industry, has seen its stock price fluctuate significantly in recent months. Rising interest rates, competitive pressures, and economic uncertainties have led to a series of pullbacks, prompting investors to question whether the current price accurately reflects the company’s value. With shares trading well below previous highs, is Affirm stock undervalued, or does it still face challenges that justify a cautious approach?

Let’s dive into the factors influencing Affirm’s current valuation and examine whether the stock presents a buying opportunity at its current price.

1. Affirm’s Valuation Metrics: Assessing the Numbers

One of the first ways to evaluate whether Affirm stock is undervalued is by examining traditional valuation metrics, such as price-to-sales (P/S) and price-to-book (P/B) ratios. Affirm, like many high-growth tech companies, has traditionally been valued based on its revenue growth and potential for future profitability. However, with the BNPL industry facing regulatory scrutiny and economic headwinds, the market has recalibrated expectations, resulting in a lower multiple for Affirm.

Currently, Affirm trades at a significantly reduced P/S ratio compared to its historical levels and its BNPL peers. This compression in valuation reflects not only the recent pullbacks in its share price but also investor concerns about the profitability of BNPL models in a high-interest-rate environment. Still, if Affirm can demonstrate resilience in its earnings and stabilize its costs, its current valuation could start to look attractive for long-term investors seeking exposure to fintech.

2. Partnerships with Industry Giants: A Growth Catalyst

One of the standout features of Affirm’s business model is its partnerships with major players like Amazon, Walmart, Shopify, and Peloton. These collaborations provide access to millions of consumers and allow Affirm to diversify its revenue streams across various retail sectors. For example, Affirm’s partnership with Amazon allows shoppers to finance purchases through installment payments directly on the Amazon platform, which significantly enhances Affirm’s transaction volume and visibility.

If these partnerships continue to drive significant revenue, they may support a bullish thesis for the stock. Affirm’s collaborations with major retailers position it uniquely compared to competitors that lack such high-profile alliances, creating a competitive moat. For investors, these partnerships could mean steady, long-term growth, helping justify a higher valuation if they continue to boost transaction volumes and attract new users.

3. Economic Headwinds and Rising Interest Rates

Despite Affirm’s growth potential, recent economic conditions have complicated the outlook for BNPL providers. Rising interest rates pose a significant challenge to Affirm, as higher rates increase its borrowing costs, potentially compressing margins. Unlike traditional lenders, Affirm does not earn interest on all of its transactions, which makes it more susceptible to fluctuations in borrowing costs when funding its loans.

Additionally, economic uncertainties have led to shifts in consumer spending, with more people prioritizing essential purchases over discretionary ones, which can affect transaction volumes on Affirm’s platform. If these macroeconomic pressures persist, they could weigh on Affirm’s ability to grow revenue and control costs, suggesting that the current valuation might still be high given the risks. However, if the economy stabilizes or interest rates eventually decrease, Affirm could see margin expansion, making the current price potentially undervalued in the long run.

4. Path to Profitability: A Critical Factor

One of the key factors influencing Affirm’s stock valuation is its progress toward profitability. While Affirm has focused heavily on growth, achieving profitability has proven challenging due to the company’s high spending on marketing and technology development, as well as the costs associated with servicing loans. Investors are increasingly focused on seeing a clear path to profitability, especially given the economic pressures on growth-oriented companies.

Affirm’s management has indicated efforts to improve operating efficiency, control costs, and refine its underwriting standards to mitigate risk. Any signs of progress in these areas, such as a reduction in operating losses or improvements in net income, could encourage investors to reevaluate the stock as a long-term buy. However, if Affirm fails to demonstrate meaningful progress toward profitability, it could continue to weigh on the stock’s valuation.

5. Regulatory Environment: A Potential Overhang

The BNPL industry has recently come under increased regulatory scrutiny, as governments and consumer protection agencies raise concerns about debt accumulation and transparency. Regulators in the U.S. and other regions are exploring potential rules for BNPL providers, which may require greater transparency, stricter credit assessments, or additional disclosure requirements.

For Affirm, any unfavorable regulatory developments could increase operational costs or limit its ability to acquire new users. However, if Affirm adapts proactively to any new regulations, it could strengthen its reputation as a responsible BNPL provider, potentially giving it a competitive edge. Regulatory risks are a significant factor in evaluating the stock’s current valuation, as new rules could either add pressure or, if well-navigated, reinforce Affirm’s standing in a regulated BNPL landscape.

6. Competitive Pressures in the BNPL Market

The BNPL sector has become increasingly crowded, with major players such as Afterpay (owned by Block, Inc.), Klarna, and PayPal competing aggressively for market share. Additionally, traditional banks and credit card companies are entering the installment payment space, which could further intensify competition. Affirm must continue differentiating its brand and product offerings to maintain its market position and sustain growth.

Despite the competition, Affirm’s strong merchant partnerships and brand recognition give it a distinct advantage. If Affirm can leverage these assets to grow its user base and retain customers, it may help justify a higher valuation. However, if it starts losing ground to competitors or faces pricing pressures, it could signal a need for caution regarding its valuation.

7. Insider and Institutional Sentiment

Another key factor that can shed light on whether Affirm is undervalued is insider and institutional sentiment. In recent months, insiders and institutional investors have shown mixed reactions to Affirm’s stock, with some increasing positions and others trimming their holdings. Positive insider sentiment, such as executives buying shares, could signal that management believes the stock is undervalued at current levels. Likewise, if major institutional investors show confidence in Affirm’s potential by adding to their positions, it could indicate that they view the current price as an attractive entry point.

Monitoring insider transactions and institutional ownership trends can provide additional insight into how industry professionals and company executives view the stock’s value, potentially reinforcing a bullish or bearish perspective.

8. Long-Term Potential vs. Short-Term Volatility

Affirm’s valuation ultimately hinges on whether investors view it as a long-term growth story or a short-term speculative play. For long-term investors, Affirm offers exposure to the broader trends in digital payments, e-commerce, and financial technology. The BNPL model continues to resonate with consumers, particularly younger generations seeking alternatives to traditional credit.

However, short-term volatility driven by interest rate fluctuations, regulatory developments, and competition presents ongoing challenges. For risk-tolerant investors with a long-term horizon, these pullbacks may offer an attractive entry point into a high-growth fintech company. On the other hand, investors seeking stability may find Affirm’s near-term challenges too risky until the company demonstrates greater profitability and resilience.

Conclusion: Is Affirm Stock Undervalued?

Affirm’s recent pullbacks have brought its stock price down significantly from previous highs, leading some investors to consider whether it’s undervalued. Affirm’s partnerships with industry giants, market position in BNPL, and efforts toward profitability make a compelling case for long-term potential. However, the company still faces headwinds from high interest rates, regulatory risks, and intense competition.

For those willing to accept short-term volatility in exchange for potential long-term gains, Affirm’s current price may indeed be undervalued, especially if the company can demonstrate progress toward profitability and continue scaling its user base through strategic partnerships. But for cautious investors, the risks associated with the BNPL sector and economic uncertainties may warrant a wait-and-see approach until Affirm proves it can adapt and thrive in a challenging environment.

In summary, Affirm may offer substantial upside for long-term investors who believe in the future of BNPL and fintech, but a careful consideration of the economic landscape and Affirm’s strategic execution will be crucial in assessing whether it’s a value buy or a speculative gamble.