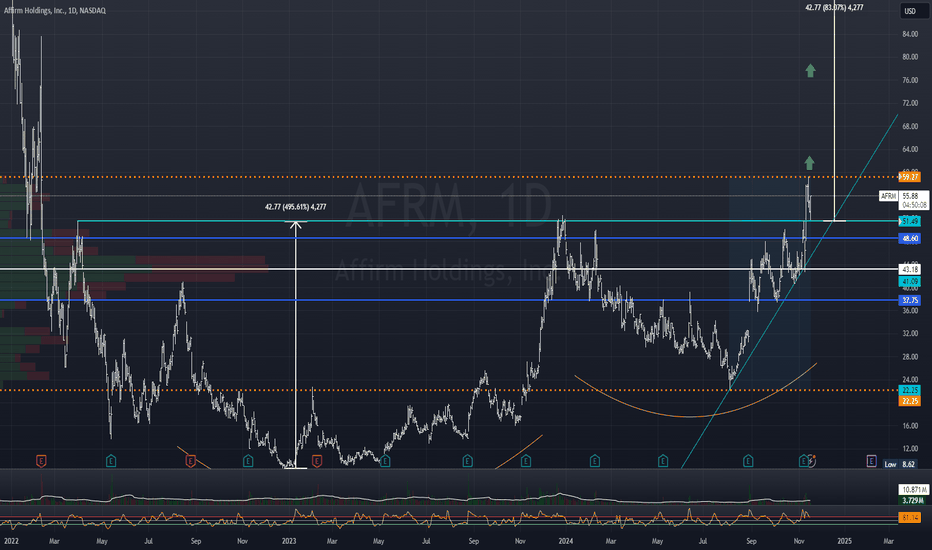

Interest rates are a critical factor in the financial landscape, influencing everything from consumer spending to stock prices. For high-growth tech companies like Affirm Holdings, Inc. (NASDAQ: AFRM), interest rates can be especially impactful, as these companies often rely on debt to fund expansion and have business models sensitive to economic fluctuations. As one of the leaders in the “buy now, pay later” (BNPL) space, Affirm’s stock performance is closely tied to interest rate trends. But how, exactly, do interest rates impact Affirm’s stock? Here’s a closer look.

1. Rising Interest Rates Increase Affirm’s Borrowing Costs

Affirm’s BNPL model allows consumers to break down purchases into manageable installments, often with no interest for the consumer. This interest-free option has made Affirm a popular choice for shoppers, especially younger consumers who are wary of traditional credit cards. However, to finance these loans and maintain liquidity, Affirm relies heavily on short-term borrowing from institutional lenders or capital markets.

When interest rates rise, Affirm faces higher borrowing costs, which can eat into its profit margins. The company’s ability to offer interest-free loans to consumers becomes more costly as the interest it pays on its own debt increases. To compensate, Affirm may either pass on some of these costs to merchants or consumers, which could reduce demand, or absorb the costs, which would compress its margins and negatively impact profitability. Either scenario has implications for Affirm’s bottom line and, by extension, its stock price.

2. Higher Interest Rates Make BNPL Less Attractive Relative to Credit Cards

As interest rates rise, the gap between BNPL services and traditional credit card interest rates can narrow. When credit card rates are relatively low, BNPL stands out as an attractive, low-cost alternative to consumers. However, as credit card rates rise alongside benchmark interest rates, BNPL may appear less unique or advantageous in comparison, potentially reducing consumer demand for installment payment options.

This shift can be detrimental to Affirm’s growth, as the appeal of BNPL could diminish in an environment where consumers are less incentivized to seek alternatives to credit cards. With fewer consumers choosing BNPL, Affirm’s revenue growth may slow, which is likely to weigh on investor sentiment and its stock performance.

3. Impact on Consumer Spending and Loan Default Risk

Interest rates have a broad impact on economic conditions, including consumer spending patterns. When rates rise, borrowing costs for consumers increase, affecting everything from mortgages to auto loans. Higher interest rates also encourage consumers to save rather than spend, as returns on savings accounts improve. For Affirm, a reduction in consumer spending directly translates to lower transaction volumes, particularly for non-essential, big-ticket items, which are common purchases made with BNPL.

Additionally, as interest rates rise, so do monthly payment amounts on variable-rate debts, like credit card balances and some types of loans. This increase in debt burden can strain consumers’ budgets, especially for lower-income households. As a result, Affirm faces a greater risk of defaults among its users, who may struggle to meet payment obligations on existing BNPL loans. If defaults rise, Affirm may incur higher losses, weakening its financial position and causing its stock to underperform.

4. Valuation Challenges for Growth Stocks in a High-Interest-Rate Environment

Affirm, like many other tech and fintech companies, is a high-growth stock that has traditionally relied on future earnings potential to attract investors. When interest rates are low, future earnings appear more valuable in present terms, making growth stocks more attractive. But as interest rates rise, investors adjust their expectations, and future earnings are discounted at a higher rate. This adjustment makes future cash flows worth less in today’s terms, often resulting in declining stock valuations for high-growth companies.

For Affirm, this valuation challenge is particularly acute because the company is not yet consistently profitable. Investors are generally more willing to accept risk and value growth potential over current profitability when interest rates are low, but rising rates make these “growth at any cost” stocks less appealing. Affirm’s stock may therefore struggle to maintain high valuations if interest rates continue to rise, as investors shift their preference toward profitable, stable companies.

5. Impact on Investor Sentiment and Market Volatility

Interest rate trends are closely watched by investors, and shifts in rates can influence overall market sentiment. Rising interest rates often signal tightening monetary policy, which can result in market volatility, especially among technology and fintech stocks. As a high-growth fintech stock, Affirm is susceptible to this volatility.

When rates rise, market sentiment often turns risk-averse, leading investors to favor safer, dividend-yielding stocks over speculative growth stocks like Affirm. This shift can create downward pressure on Affirm’s stock price as investors rebalance their portfolios, moving away from riskier assets. Additionally, market volatility may amplify reactions to Affirm’s earnings reports, guidance updates, and other major announcements. Positive or negative news can drive larger-than-expected price swings in a volatile, interest-sensitive market, increasing short-term risk for Affirm’s shareholders.

6. Possible Strategies to Offset Rising Interest Rate Impact

Affirm has some options to navigate the challenges of a rising interest rate environment:

- Product Diversification: Expanding beyond BNPL into other financial services can help Affirm diversify its revenue streams and reduce reliance on a single product. For example, Affirm has launched high-yield savings accounts and hinted at potential plans to expand into additional lending products. This approach could allow Affirm to offset some of the pressures of rising borrowing costs by offering complementary services.

- Targeting High-Quality Borrowers: Tightening its lending standards to focus on higher-credit consumers may help Affirm reduce default risk and maintain profitability as interest rates rise. While this may limit growth, it can ensure that the loans Affirm underwrites are lower-risk, potentially protecting its bottom line in challenging economic conditions.

- Merchant Partnerships and Revenue Sharing: Affirm can explore ways to shift some of its financing costs to its merchant partners. By sharing revenue with merchants or adjusting terms to reflect the impact of higher interest rates, Affirm could help offset some of the increased borrowing costs.

- Exploring International Markets: Expanding into international markets with lower interest rate environments could help Affirm diversify its risk exposure. Regions with different monetary policies or consumer behavior patterns may provide growth opportunities less affected by U.S. interest rate fluctuations.

Conclusion

Affirm’s business model and stock performance are closely linked to interest rate trends, which impact its borrowing costs, consumer demand, and valuation. In a low-interest-rate environment, Affirm’s BNPL offering is compelling and cost-effective. However, as rates rise, Affirm faces multiple pressures: increased borrowing costs, reduced consumer spending, a higher risk of loan defaults, and lower growth valuations.

To thrive in a higher-rate environment, Affirm will need to adapt by diversifying its product offerings, targeting lower-risk borrowers, and exploring international opportunities. For investors, Affirm’s stock represents both potential and risk—successfully navigating rising interest rates could solidify its long-term potential, while failure to adapt could make it vulnerable to significant downturns. For now, monitoring interest rate trends and Affirm’s response to them will be crucial for investors evaluating AFRM as either a short-term trade or a long-term growth opportunity.