The “buy now, pay later” (BNPL) industry has gained tremendous popularity, and Affirm Holdings, Inc. (NASDAQ: AFRM) stands as one of its prominent players. Since going public in early 2021, Affirm has both thrilled and tested investors with its volatile stock performance. If you’re considering adding Affirm to your portfolio, it’s essential to dive into the company’s financials, growth prospects, market positioning, and the challenges it faces.

What Does Affirm Do?

Affirm offers point-of-sale financing that allows consumers to pay for purchases over time without traditional credit cards. Instead of charging late fees or compounding interest like many credit card companies, Affirm charges simple interest and focuses on transparency. The company’s BNPL model has resonated particularly well with younger consumers, who are wary of credit card debt but still want flexible payment options.

Key Strengths: Why Affirm Could Be a Good Investment

- Partnerships with Major Brands and Merchants

Affirm has partnered with popular brands and large-scale retailers like Amazon, Shopify, and Walmart. These partnerships provide substantial visibility and credibility, placing Affirm’s services directly in front of millions of potential users. Its exclusive deal with Amazon, in particular, gives Affirm a unique advantage in the competitive BNPL landscape. - Strong Growth Potential in BNPL

The BNPL market is expected to grow significantly over the next decade as consumers continue to seek alternatives to traditional credit cards. In a report from Research and Markets, the BNPL industry was valued at around $90 billion in 2020, with projections to grow at a compound annual growth rate (CAGR) of over 20% until 2028. Affirm is well-positioned to capitalize on this trend. - User-Friendly Technology and Data Insights

Affirm’s data-driven technology allows it to assess a consumer’s ability to repay before granting a loan, helping to manage risk and reduce loan defaults. The user-friendly interface and mobile-first approach also appeal to tech-savvy consumers who prioritize convenience and transparency. - Expanding Services Beyond BNPL

Affirm has begun to offer financial services beyond the basic BNPL model, such as savings accounts and interest-bearing products. This diversification could support revenue growth and potentially shield the company from future market downturns within the BNPL segment alone.

Key Risks: Why Investors Should Exercise Caution

- Regulatory Uncertainty

As BNPL platforms grow in popularity, regulators worldwide are taking notice. Both U.S. and international regulatory bodies are examining the potential risks of BNPL, which could lead to new rules and restrictions. Increased regulation could hinder Affirm’s business model, particularly if it imposes caps on fees or requires more stringent underwriting practices. - Dependence on Key Partnerships

While Affirm’s partnerships with Amazon, Shopify, and other major retailers are a competitive advantage, they also present a risk. Losing a partnership with a major brand like Amazon could significantly impact Affirm’s revenue, user base, and market valuation. - Rising Competition in the BNPL Space

The BNPL industry has attracted numerous competitors, including Klarna, Afterpay, and even established tech giants like PayPal. Increased competition could squeeze margins, force Affirm to offer less favorable loan terms, or result in higher customer acquisition costs. Additionally, some traditional banks are now exploring BNPL products, which may intensify competition further. - Profitability Concerns

Like many high-growth tech companies, Affirm has yet to achieve consistent profitability. The company has made substantial investments in growth, but investors should be aware that Affirm’s bottom line may remain under pressure in the near term. Its financial performance could be negatively impacted if the BNPL industry’s growth rate slows or if competition pressures its pricing model. - Interest Rate Sensitivity

Affirm’s business model relies heavily on financing purchases through loans, making it sensitive to interest rate fluctuations. In a rising interest rate environment, the cost of borrowing for Affirm could increase, which could compress its margins. Higher interest rates may also reduce consumer spending, which would impact Affirm’s transaction volume.

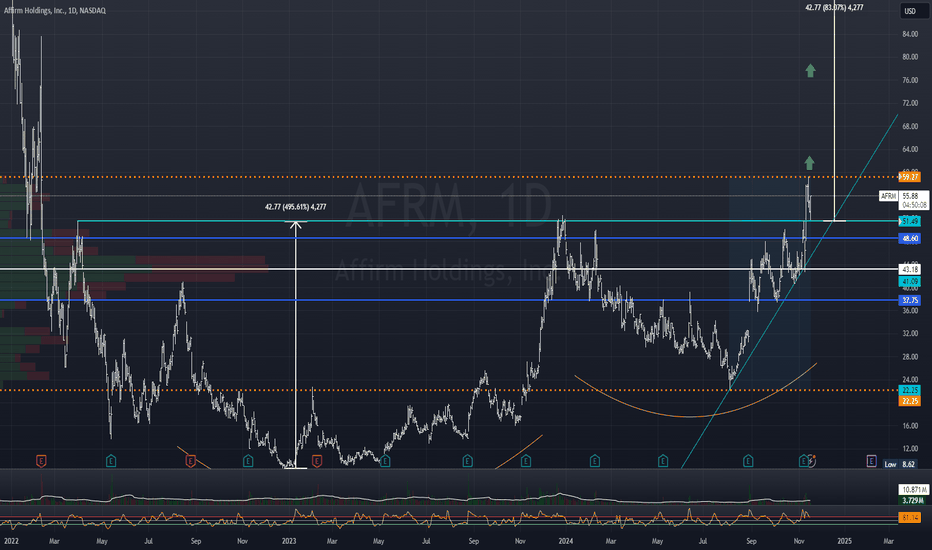

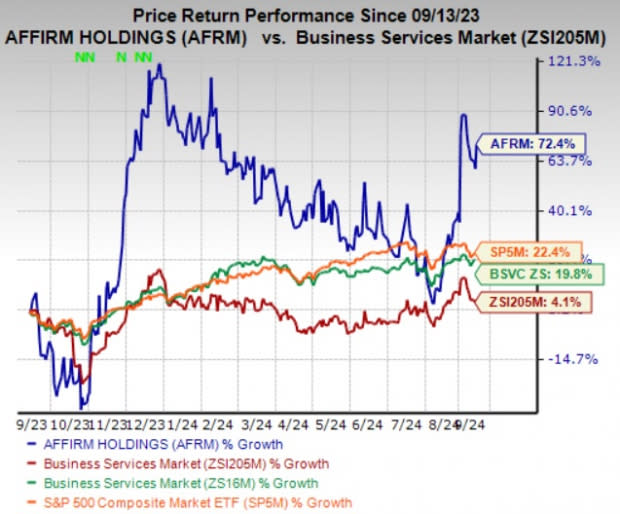

Financial Performance: Mixed Results

In recent quarters, Affirm has reported strong revenue growth, but profitability remains a challenge. As of its latest earnings report, the company’s revenue increased year-over-year, yet it still operates at a loss. Affirm’s growth in gross merchandise volume (GMV) is promising, but with rising costs and increasing competition, reaching profitability may require further strategic adjustments.

Analyst Opinions on Affirm

Analysts have mixed views on Affirm’s stock. Some remain optimistic, pointing to the company’s growth trajectory, valuable partnerships, and strong brand recognition as positive indicators. However, other analysts highlight Affirm’s lack of profitability and exposure to economic cycles as significant concerns.

Most analysts agree that Affirm has considerable long-term potential, especially if it can successfully execute on its growth strategies. But for investors focused on short-term gains, the stock may be too volatile and dependent on external factors, like regulation and interest rates, to offer stable returns in the near term.

So, Is Affirm a Buy?

Ultimately, whether Affirm is a buy depends on your investment strategy, risk tolerance, and time horizon.

- For long-term growth investors, Affirm’s position in a rapidly expanding industry could make it an attractive high-risk, high-reward investment. If Affirm continues to grow its user base, maintain its partnerships, and expand its financial services offerings, it could become a leader in the evolving digital finance space.

- For more conservative investors, the current risks, including regulatory uncertainty and Affirm’s unproven path to profitability, may be too significant. These investors might consider waiting until Affirm shows a consistent record of profitability or until regulatory concerns in the BNPL industry are clarified.

- For value investors, Affirm’s current valuation may appear too high relative to its earnings potential. Waiting for a more attractive entry point, possibly during a period of market or sector weakness, could be a safer approach.

Final Thoughts

Affirm offers a compelling growth story in the BNPL sector, but it is not without significant risks. With the BNPL industry poised for growth but also facing regulatory and competitive headwinds, Affirm’s future success will largely depend on its ability to adapt and expand beyond its core offerings. Investors should weigh these factors carefully and consider their risk tolerance before making a decision.

As always, conducting further research and consulting with a financial advisor can help investors make a more informed decision about adding Affirm (AFRM) to their portfolio.