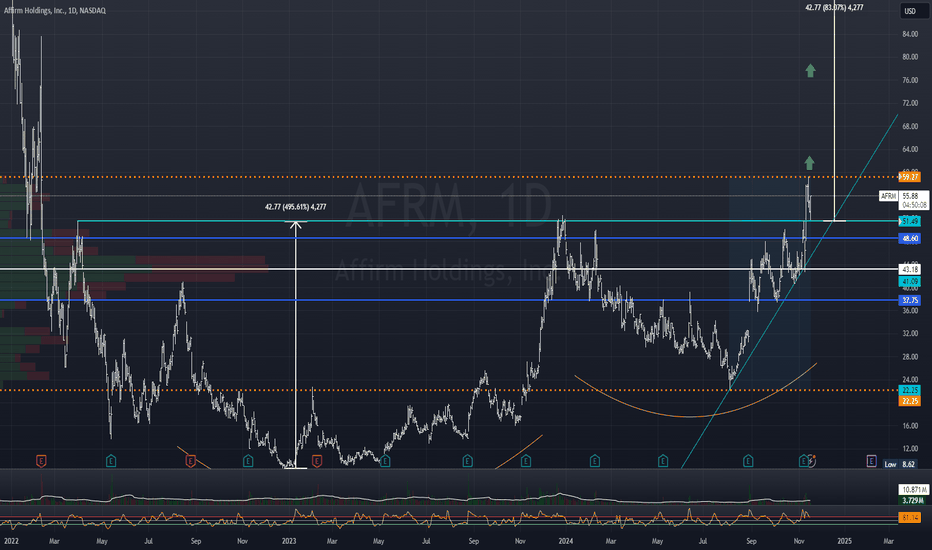

Affirm Holdings (NASDAQ: AFRM) operates in the heart of the Buy Now, Pay Later (BNPL) sector, a market fueled by consumer demand for flexible payment options. As the company provides consumers with the ability to break up purchases into manageable, interest-free installments, its financial health and stock price are heavily influenced by shifts in consumer spending behavior. In this article, we’ll explore how consumer spending trends affect Affirm’s stock, why these trends are important to investors, and what potential signals investors should watch for in the coming months.

1. The Link Between Consumer Spending and BNPL Growth

At its core, Affirm’s business model hinges on consumer spending. The company makes money by facilitating loans for consumers to make purchases at partner retailers, earning fees from both consumers and merchants. As a result, the volume of transactions processed through Affirm’s platform directly correlates with consumer purchasing behavior.

In a growing economy where consumer confidence is high, people tend to spend more, often on larger-ticket items like electronics, furniture, and even travel experiences—categories where BNPL services like Affirm are commonly used. During such periods, Affirm sees a rise in transactions, which in turn drives revenue growth.

However, if consumer sentiment weakens or spending slows due to economic factors, Affirm’s revenue may be directly impacted, as fewer consumers will be using BNPL services for their purchases. Thus, Affirm’s stock is highly sensitive to the overall direction of consumer spending trends.

2. The Role of Consumer Confidence in Shaping Spending Patterns

One of the key indicators of consumer spending is consumer confidence. When consumers feel optimistic about their financial future—whether because of rising wages, low unemployment, or a stable economic outlook—they are more likely to spend. This increase in spending activity typically leads to higher demand for BNPL services, as consumers take advantage of flexible payment plans offered by companies like Affirm.

Conversely, in times of economic uncertainty—such as during recessions or periods of high inflation—consumer confidence can take a hit. In these environments, consumers tend to be more cautious with their spending, preferring to save rather than spend. This shift in behavior can have a cooling effect on BNPL companies like Affirm, as fewer people may be inclined to take on debt or opt for installment payments during uncertain times.

For example, during the COVID-19 pandemic, Affirm saw a surge in demand for BNPL services as consumer habits shifted toward online shopping and more flexible payment options. But in periods when consumer confidence is low, Affirm may face challenges as spending slows.

3. Economic Slowdowns and Rising Interest Rates: Potential Threats to Consumer Spending

Affirm’s performance is also closely tied to macroeconomic factors that influence consumer spending, particularly interest rates. When interest rates rise, as they have in recent years in response to inflation concerns, borrowing becomes more expensive. For consumers, higher interest rates can lead to higher monthly payments on loans, including those offered through BNPL services. As a result, consumers may opt for lower-value purchases or delay spending altogether, especially on discretionary items.

Moreover, an economic slowdown or recessionary environment can further dampen consumer confidence, leading to reduced spending. In such situations, Affirm may experience a decline in transaction volume and revenue, as consumers may either avoid large purchases or prefer to pay with cash to avoid taking on new debt.

The current economic landscape, with rising interest rates and inflation, has created uncertainty for both consumers and businesses. If these trends persist, Affirm’s stock price could face downward pressure as the company experiences slower growth and higher credit risk.

4. The Impact of Shifting Demographics on Consumer Behavior

Affirm’s core customer base includes younger consumers, particularly millennials and Gen Z, who are more likely to use BNPL services due to their preference for flexible payment options. As these generations become a larger segment of the consumer market, their spending patterns will significantly impact Affirm’s growth.

These younger consumers tend to prioritize experiences and lifestyle products over traditional goods, and they favor online shopping over in-store purchases. This shift toward digital shopping and the preference for flexibility in payment options plays directly into Affirm’s strengths. As the younger generation continues to dominate consumer spending, Affirm could benefit from continued adoption of BNPL services, especially if consumer trends remain favorable.

However, it’s important to note that consumer behavior is not static. Shifts in preferences or behaviors—such as a move away from online shopping or greater reluctance to take on debt—could hurt Affirm’s revenue stream. Investors should monitor how Affirm’s target demographic evolves over time and how the company adapts to these changes.

5. Seasonal Spending Trends and Their Impact on Affirm

Another key aspect of consumer spending that affects Affirm is the seasonal nature of retail spending. Certain periods of the year, such as the holiday season, back-to-school shopping, or summer sales, often lead to a spike in consumer purchases. These peaks in spending can significantly boost Affirm’s transaction volume, as shoppers take advantage of BNPL to manage larger purchases.

During these high-demand periods, Affirm typically sees an uptick in new customer sign-ups, larger transaction sizes, and higher conversion rates. Conversely, in slower periods of the year when consumer spending typically dips, Affirm may experience a slowdown in transactions and revenue.

The company’s ability to manage seasonal fluctuations and align its marketing and partnerships to take advantage of these peaks in consumer spending is crucial. This is also a time when investors should keep an eye on Affirm’s quarterly earnings reports to see if it is meeting seasonal expectations and maintaining strong growth in these key periods.

6. The Effect of Consumer Debt Levels on BNPL Usage

While BNPL services like Affirm are popular among consumers, the increasing levels of consumer debt could affect future spending trends. As consumers take on more debt, whether through credit cards or installment loans, their capacity to take on additional financing may diminish. If consumers begin to feel the weight of their existing debt, they may become more cautious about using BNPL services or may prioritize paying off existing loans over making new purchases.

Additionally, as the regulatory landscape around BNPL companies tightens, Affirm could face additional scrutiny over lending practices, potentially impacting its ability to serve certain consumer segments or increasing the cost of doing business. This regulatory risk, combined with rising debt levels, could dampen consumer enthusiasm for BNPL products, leading to slower growth in transaction volume.

7. What Investors Should Watch For: Signals in Consumer Spending

For investors tracking Affirm’s stock, there are several key signals related to consumer spending that can help determine the company’s future performance:

- Consumer Confidence Indices: Regular updates on consumer confidence, such as the University of Michigan’s Consumer Sentiment Index or the Conference Board’s Consumer Confidence Index, can provide insight into how willing consumers are to spend and take on debt.

- Retail Sales Data: Reports on retail sales, especially e-commerce trends, will provide a snapshot of overall spending activity and consumer behavior. Affirm’s growth is tied to both online and in-store retail sales, so this data is critical.

- Interest Rate Changes: The Federal Reserve’s decisions on interest rates are a crucial factor in consumer spending and borrowing behavior. A rise in interest rates could signal slower spending and a potential drag on Affirm’s growth.

- Debt Levels and Default Rates: Monitoring trends in consumer debt levels and the default rates on BNPL loans will give investors a sense of the risk environment Affirm is operating in. A rise in defaults or a shift toward more conservative borrowing could affect Affirm’s profitability.

8. Conclusion: How Consumer Spending Shapes AFRM Stock

Affirm’s stock price is closely tied to the dynamics of consumer spending. As a company built on facilitating consumer purchases through installment payments, any shifts in consumer behavior, confidence, or economic conditions can have significant impacts on its financial performance. Positive trends in consumer confidence, a strong retail environment, and increased adoption of BNPL services can drive Affirm’s stock price higher. However, in times of economic uncertainty or rising debt levels, the stock may face downward pressure.

For investors, understanding the underlying trends in consumer spending, watching for signals of economic slowdowns, and being mindful of shifting demographic preferences will be key to making informed decisions about Affirm’s stock. While Affirm holds a promising position in the rapidly evolving BNPL market, it remains vulnerable to broader economic and consumer trends that could influence its growth trajectory.